The sizable pandemic mortgage refinance enhance is most certainly over, nonetheless the aftershock is unexcited rippling via the housing market. Householders are retaining up dwelling sales, as their extremely-low prize is simply too treasured to present up.

For the length of the early days of coronavirus pandemic in 2020 and 2021, mortgage charges fell sharply, and hundreds and hundreds of homeowners jumped at the different to refinance. The 30-three hundred and sixty five days mortgage fell all the plan down to 2.65% in early January of 2021, based fully on Freddie Mac records

FMCC,

-0.13%.

The Federal Reserve Bank of Contemporary York estimated that 14 million mortgages were refinanced right via the “pandemic refinancing enhance.”

The surge in refinancing changed into once, in phase, attributable to sturdy family balance sheets and an increased need for housing, the Contemporary York Fed said in a blog post published Monday.

The frequent homeowner who refinanced saw their monthly price drop by $220, the Fed said.

The finest share of mortgages that were refinanced originated from 2015 onwards, the NY Fed. said. Older mortgages, corresponding to those originated sooner than 2010, were the least at probability of be refinanced.

Householders most at probability of refinance their mortgage owed a balance of $400,000 to $500,000 on their mortgage, the NY Fed concluded.

“The mortgage refinancing enhance is over, nonetheless its impact will be considered for decades to come aid,” Andrew Haughwout, director of family and public coverage analysis at the NY Fed, said in a press release.

Extremely-low charges maintain squeezed housing inventory

One among the finest penalties of the refinancing enhance is that might maybe maybe maybe-be homebuyers right this moment are if truth be told struggling to search out homes in the marketplace.

“The tip of essentially the most most modern exceptionally low interest-charge length leaves homeowners significantly disincentivized to sell or commerce properties,” the NY Fed authors popular.

In other phrases, homeowners aren’t spirited about giving up their extremely-low mortgage charge and selling their dwelling. No longer finest are charges some distance better right this moment, with the 30-three hundred and sixty five days above 6%, nonetheless dwelling costs maintain persevered to cease elevated.

Contemporary listings — what number of sellers were striking up their homes in the marketplace — were down by 16% in early Would possibly maybe also honest when put next to a three hundred and sixty five days prior to now, based fully on Realtor.com.

(Realtor.com is operated by News Corp

NWSA,

-1.01%

subsidiary Pass Inc., and MarketWatch is a unit of Dow Jones, furthermore a subsidiary of News Corp.)

“Householders now having a peek to switch will face increased borrowing costs and better costs, with most modern dwelling costs being more than 36% better than they had been pre-pandemic,” the NY Fed said.

Householders seem reluctant to sell. Sales of previously-owned homes fell 22% three hundred and sixty five days-over-three hundred and sixty five days in March, based fully on the National Association of Realtors. Contemporary records on April dwelling sales will be launched this week.

Many shoppers are turning to recent builds to search out horny housing alternatives. Contemporary dwelling sales jumped 9.6% in March. One-third of housing inventory is recent construction, a deviation from the historic norm of most modern homes being upright 10% of overall housing, the National Association of Dwelling Builders said in April.

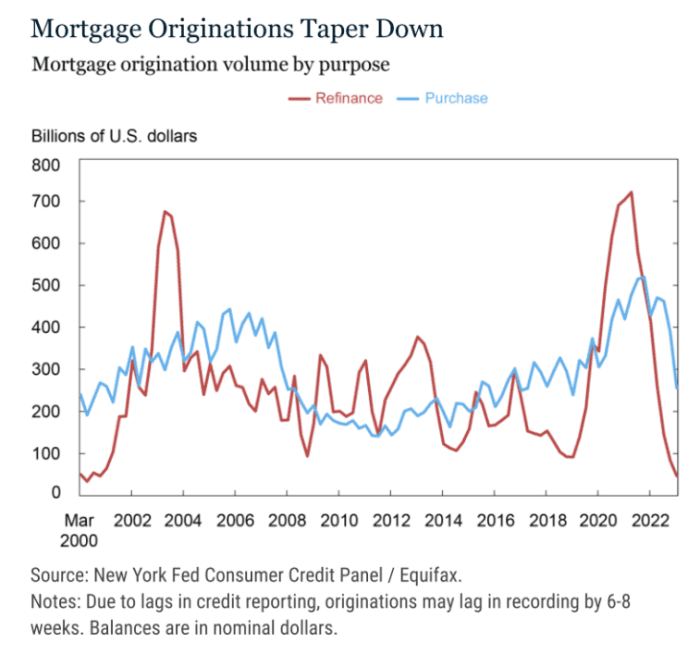

And for the mortgage industry, enterprise is at probability of be some distance slower than it changed into once right via the pandemic as fewer homeowners are refinancing. The NY Fed said mortgage originations — which embody refinanced mortgages — fell sharply in the predominant quarter of 2023 to $324 billion, the bottom level since 2014

It’s no longer tough to note why few are attracted to refis: The 30-three hundred and sixty five days changed into once averaging at 6.35% in mid-Would possibly maybe also honest, as when put next to 5.3% a three hundred and sixty five days prior to now, based fully on records from Freddie Mac.

The upward thrust in charges between December 2020 and October 2022 changed into once no longer upright steep, it changed into once historic: Charges rose from 2.68% in 2020 to 6.9% in 2022, the finest swing for the reason that early Nineteen Eighties, the NY Fed said, citing records from Freddie Mac.